Correctly planted trees enhance homes, save energy

David M. Brown, Special for The Republic | azcentral.com

For energy savings and comfort in the desert, trees have us covered.

Most Valley residents didn’t attend the Regional Tree & Shade Summit 2.0 in Phoenix on March 9, but a full house of 180 people had their schedules highlighted in green to ensure they were there.

With a keynote address by Dr. Greg McPherson, research forester for the U.S. Department of Agriculture’s Pacific Southwest Research Station in Davis, Calif., the second summit attracted public and private companies and individuals interested in local urban forests, low impact development and increasing the success of tree and shade efforts by cities and property owners.

Benefits to homeowners

Homeowners can benefit from lifestyle enhancement and energy savings by correctly planting trees, said Anne Reichman, CSBA, program manager for the Sustainable Cities Network at GIOS. The event was held at the Downtown Phoenix ASU campus.

For one, trees are important to the health, vitality and beauty of our communities.

“Research shows that the prevalence of trees is linked to safer neighborhoods, less urban heat island effect and increased property values,” she said.

In addition, trees bring people together.

“In speaking with various attendees at the summit, it was amazing how many people had their own stories or memories associated with a special tree or area with trees,” Reichman said. “They provide a connection with the environment, and, more importantly, with other people and experiences within our individual lives. Trees create memories or backdrops for those memories.”

For instance, in his opening remarks to the group, Avondale Mayor Kenn Weise spoke about his home town, Chicago, and its commitment to increasing urban forestry efforts.

And, trees are “solutions multipliers”: “They provide multiple benefits in the area of air quality, removing pollutants from our air, reducing stormwater run-off and energy-related costs in residential buildings and providing valuable shade in our hot desert environment,” Reichman said.

Savings to Phoenix

For instance, the city of Phoenix estimates that trees reduce energy-related costs from residential buildings in the city by $22.9 million annually reduce storm water runoff by 91.7 million cubic feet per year and $6.11 million per year, she said, citing city figures.

“The 3.2 million trees comprising Phoenix’s urban forest are a $3.8-billion asset that provides $40 million in annual services by reducing cooling costs, cleaning the air, reducing stormwater runoff, storing carbon, increasing home sales prices and promoting human health and well-being,” said McPherson, who has studied the value of trees to urban forest planning and management.

“Trees are a valuable asset not for the property owner but the community,” said Richard Adkins, forestry supervisor, city of Phoenix Parks and Recreation. “They are a low-cost, high-yielding investment, supplying environmental, economic and social/health benefits.”

As an investment

For instance, just one correctly planted mesquite tree reaps a 40-year benefit of $2,755 for its energy effects, carbon storage, air-pollutant uptake, rainfall interception, stormwater-runoff reduction and property value increase, McPherson said.

“Trees are an important investment for both cities and residents in that they provide short- and long-term benefits when properly valued, maintained and cared for,” Reichman said.

Phoenix does this through its Master Tree & Shade Plan 2030.

Glendale and Mesa have partnered on a Water Infrastructure Finance Authority to create a Low Impact Development Toolkit for Valley cities to divert stormwater for use in the plants/trees, increasing their long-term survival without the need for irrigation.

The city of Avondale adopted its Street Tree Master Plan in December 2014.

“One of the primary points of the summit was to provide continuing education to those like me tasked with maintaining the urban forest, so our neighbors will benefit knowing that urban foresters have connected and are planning for the future in terms of tree canopy, maintenance, master planning and other components,” said Drew Bryck, the city’s environmental program manager.

Getting them in the ground — correctly

The city of Tempe’s principal planner, architect Bonnie Richardson, said the need for eduction and action in getting trees in the ground now for future generations was a theme of the summit.

“Planting the right tree, in the right place, is a legacy of value as well as beauty,” she said.

The city is completing an Urban Forestry Master Plan & Action Plan.

Trees are often planted incorrectly, however, leading to shorter natural lifespans or issues requiring removal, Reichman said.

To correct this, Salt River Project discussed the benefits of its Shade Tree Program, administered by Valley Permaculture Alliance, which also attended.

The popular program offers up to two free desert-adapted trees to SRP residential customers who attend a 70-minute workshop about how to best plant and care for their new trees.

“Well-placed shade trees can reduce cooling needs by 10 percent by blocking the sun’s rays,” said Lori Rogers, SRP Residential Energy Efficiency Program marketing manager. “The side of the house shaded by the tree can be 10 degrees to 30 degrees Fahrenheit cooler at peak times — all without using a lot of water.

“In addition to saving up to $50 annually on cooling costs, shade trees also add value to customers’ property, produce oxygen to help clean the air, provide a wildlife habitat and reduce stormwater runoff.”

Summit details

The summit included sessions and discussions on topics including municipal planning, the role of trees in green infrastructure, municipal ordinances, health benefits of trees, biogenic volatile organic compounds, municipal urban forestry planning, species selection, sustainable maintenance and the benefits of structural shade in areas not suitable for tree placement.

The event was hosted in partnership with ASU’s Sustainable Cities Network and the Julie Ann Wrigley Global Institute of Sustainability, the cities of Avondale, Mesa, and Phoenix, Downtown Phoenix, Inc., the Arizona State Forestry Division, and USDA Forest Service.

Funds were provided by the Urban and Community Forestry Financial Assistance Program administered through Arizona State Forestry — Urban and Community Forestry Program and the USDA Forest Service.

“We loved Dr. McPherson’s comment that trees are the most efficient organism on the planet,” Mesa resident Marquetta White, who attended with husband Bob. “He also pointed out that trees are vital to health, improving our mental, emotional and physical well-being.”

If you’ve ever bought a house, you were probably given the opportunity to buy a home warranty in conjunction with the purchase.

Home warranties are some of the most-marketed products in real estate, and often come with referral bonuses. But are they worth it?

In my experience as a homeowner and landlord, I’ve had contracts with four of this country’s leading providers. I’ve learned that it’s a game of risk vs. reward and value vs. cost.

It’s a game of risk vs. reward and value vs. cost

This article discusses the common questions and concerns regarding home warranties, including:

What is a home warranty?

What is covered?

How much do they cost?

Are they worth it?

What Is a Home Warranty?

Simply put, it’s a home services contract that will pay for necessary repairs due to common maintenance issues, and for the subsequent replacement of appliances if they cannot be repaired.

The home warranty industry was started in 1971 by American Home Shield and has grown into a competitive nationwide industry occupied by dozens of companies. However, it’s important to realize that though these policies are called “warranties” they are not actually warranties in the common sense of the term.

It’s Not Actually a “Warranty”

A traditional “warranty” in the general sense, is a guarantee towards the quality of a product or service made by the seller to the buyer.

A “home warranty” is not a guarantee, but rather a contract to provide repair and/or replacement services for major appliances and home systems that fail due to normal wear and tear.

These service contracts will not cover every repair or issue that you may have.

In fact, common consumer complaints show that many of these companies try to evade coverage by citing homeowner’s maintenance negligence or claiming the issue is a “pre-existing problem.”

Angie Explains

What Does the Policy Cover?

Typical basic policies cover home appliances, heating, cooling, plumbing, and electrical systems.

For a premium, most providers will cover roofs, wells, pools, plumbing and lighting fixtures, and lawn sprinkler systems.

Structural systems are not typically covered under a home warranty policy, but rather by a traditional primary home insurance policy.

Common Coverages

Repair Item

Basic Plans

Premium Plans

Refrigerator

X

X

Built-in Microwave Oven

X

X

Stove/Oven

X

X

HVAC (Heating/Cooling)

X

X

Electrical System

X

X

Cooktop

X

X

Plumbing System

X

X

Clothes Washer/Dryer

X

X

Garbage Disposal

X

X

Ductwork

X

X

Ceiling Fans

X

X

Plumbing Stoppage

X

X

Water Heater

X

X

Clothes Dryer

X

X

Garage Door Opener

X

X

Dishwasher

X

X

Pool

X

Sum Pump

X

Stand Alone Freezer

X

Ice Maker

X

Central Vacuum

X

Well Pump

X

Lawn Sprinkler System

X

Plumbing Fixtures

X

Lighting Fixtures

X

Roof

X

Septic Systems

X

Water Filters

X

Always Read the Fine Print

Actual coverage varies significantly between the plethora of home warranty companies. Most companies will promise you the world, but many consumers often find that their contracts are riddled with exclusions and denial provisions.

For example, most basic policies include plumbing, but not if the pipes freeze.

Further, the actual parts that tend to break most often, like a shower diverter or sink faucet, are not covered at all. When the contract refers to “plumbing,” they only mean the actual pipes in the wall.

It’s important to remember that home warranty companies are for-profit entities and they will pursue their best interests, not yours.

Home warranty companies are for-profit entities

and they will pursue their best interests, not yours.

Check the Maximum Allowances

Though “heating” is typically covered with the option to replace the furnace should it not be repairable, the contract might specify that the insurer will only pay up to $1,000 toward a replacement, at their option.

Though helpful, most furnaces cost between $3,000-$7,000, leaving the consumer to pay the difference.

Further, the homeowner does not get to choose whether it’s time to replace the unit or not. The warranty company could opt to issue a payout, and let the homeowner deal with it alone.

By that point, the furnace has been broken for at least a week, the tenants are asking for a rent refund, and the policy holder must coordinate the repair with another service company.

How Much Do They Cost?

Besides Cozy, it’s hard to find products that provide incredible value at little or no cost. Like most warranty and insurance products, the cost of a policy depends on the amount of coverage you buy.

Again, most companies have both basic and premium policies that you can purchase, but they will all insure specific items, such as hot tubs or solar panels, for an extra fee.

Annual Fee

In my experience, policies range from $400-$800 per year for a typical single-family home, depending on the amount of coverage that is purchased.

Most companies will validate their price by providing cost-comparison charts of common repairs, such as the one below, but fail to mention the maximum payouts or exclusions previously mentioned.

Item

Average Replacement Cost

Average Repair Cost

Cost w/ Home Warranty

Central A/C

$4,013

$535

$100 service fee

Heating System

$3,000

$685

$100 service fee

Refrigerator

$1,025

$308

$100 service fee

Plumbing

$1,100

$363

$100 service fee

Range/Oven

$1,400

$180

$100 service fee

Washer or Dryer

$525

$180

$100 service fee

Source: Estimates are based on national independent service contractors

Though such comparisons are mostly accurate, the dirty little secret of the insurance industry is that these companies make their money because they know most people don’t fully utilize the service.

…they know most people don’t fully utilize

the service.

Deductible/Service Call Fee

The most common deductible for home warranty policies come in the form of a service fee.

When a repair technician shows up to inspect and service the property, the policy holder is responsible for providing a small payment directly to the technician, regardless of the work being performed.

In my experience, this deductible typically ranges from $75-$150 per claim. HMS National has the only policy that I’ve seen with a $0 deductible, however their premiums are slightly higher. Perhaps it balances out in the wash (pun intended).

Waiting Period

Most companies contractually have a 30-90 day waiting period between signing up and when the consumer can actually use the service.

This waiting period is designed to prevent a policy holder from making a claim on a pre-existing condition, but I think it is a horrible way to start out a new business relationship.

It’s like saying “Yes, you must pay the bill, and no, you can’t use the service yet.” Can you imagine if car dealerships made you pay for a car, but then you couldn’t drive it for 90 days?

Yes, you must pay the bill, and no, you

can’t use the service yet!

These waiting periods can be quite frustrating when a new repair issue surfaces prior to the waiting period ending – leaving the policy holder to seek help elsewhere. What a bad first impression!

Is a Warranty Worth Buying?

Whether or not you choose to buy a home warranty is a personal decision based on multiple factors.

Personally, I typically purchase a home warranty for the first 1-2 years on every property that I acquire.

After a few years, I usually feel that I have a better understanding of the status and condition of the home and its appliances, and usually choose to self-insure repairs via an emergency fund from that point on.

Written by Jane Meggitt from Landlordology

The rules for handling and deducting from a security deposit are commonly misunderstood. This article will clarify the legitimate reasons for withholding all or part of a security deposit from a tenant.

Best Practices for Withholding a Security Deposit

It’s a common scenario: your tenant pays you a security deposit before moving in, which gives you some peace of mind that the money will pay for certain items or damages when the tenant moves out.

When move-out day arrives, the tenant says they left the unit spotless, but the floor wasn’t even swept. Or worse, there are broken windows, an unidentifiable sticky liquid all over the fridge, and a clogged shower.

…only withhold deposit monies for actual

damages, material or financial.

The general rule is that a landlord or manager can only withhold deposit monies for actual damages, material or financial. Meaning, you can deduct money if they owe you past due rent and fees, or caused damages beyond normal wear-and-tear.

State laws vary greatly, but there are generally some statues that regulate the basics such as:

whether or not you must put the money into an interest-bearing account,

if you can or cannot commingle such deposits with your personal or business accounts

what you can or can’t deduct from a tenant’s security deposit

the timeframe in which you must return the deposit or supply written notice of why you aren’t returning all or part of it.

Things to Remember:

Always fill out an “Inventory/Condition Checklist” before the tenant moves-in so that there is a baseline for comparison.

Provide the tenant with an itemized receipt of any deductions before returning any money.

Take plenty of pictures of the damages and overall condition after each move-out.

Follow your state’s rules and timelines for returning the deposit.

Let’s talk about some basic general rules for deducting and withholding deposits.

Breaking the Lease

You can’t automatically keep a deposit just because your tenant abandons the lease or breaks a rule in it. Again, you must have actual damages to offset your claims against the deposit.

If the tenant leaves you high and dry with unpaid rent, utility bills, late fees, and parking fees, then you could withhold some or all of the deposit to cover the debt. A lease is a contract, and if the tenant breaches it, you can take them to court if they don’t pay.

Practically speaking, unless the debt is multiple thousands of dollars, going to court is often more trouble than it’s worth. Even if you receive a judgment, you still have to collect it from the former tenant. Most landlords opt to keep the security deposit and look for a suitable new tenant.

Abandonment and Unpaid Rent

If the tenant abandons the lease and stops paying rent, you almost certainly will have a claim because it takes a few weeks, if not months, to find a replacement tenant. Your previous tenant would still be responsible for rent during that time, and if he/she didn’t pay, then you could withhold the deposit to offset the unpaid rent, and sue them for any remaining balance.

Note: if you keep a month’s worth of rent from the deposit, but don’t actually have a vacancy that is a month-long, then you would need to give back any overlapping funds.

You can’t “double dip” on the rent! Do the right thing!

Since most security deposits cover only one or two month’s rent, it’s important to start eviction proceedings as soon as possible if the tenant makes no attempt to pay.

If you’re not familiar with the eviction process in your area, hiring an attorney is wise. It’s not okay for the tenant to forego paying the final month’s rent under the assumption you’ll apply the security deposit to it – so don’t use the deposit for last month’s rent.

Normal Wear and Tear

Every property suffers some normal wear and tear, and you can’t deduct that basic upkeep from the security deposit. If the tenant cleans regularly, then the landlord is always responsible for normal wear and tear.

The general rule of thumb is that a landlord is not allowed to deduct from the tenant’s security deposit for “normal wear and tear”.

Normal wear and tear typically includes the following:

General rug wear

Sun-faded wallpaper or paint

Nail holes in walls from picture hangings

Bathroom mirror desilvering

Appliances no longer working, but not due to misuse

Warped windows or doors, due to temperature or age

Dirty draperies or blinds

Texas, as well as other states, define “normal wear and tear” as:

“…deterioration that results from the intended use of a dwelling…but term does not include deterioration that results from negligence, carelessness, accident or abuse of the premises, equipment or personal property by the tenant, by a member of the tenant’s household or by a guest of the tenant.”

Meaning, if a tenant was simply living in the property the way it was intended, and did not damage anything by means of abuse, negligence, accident, guests, animals, or lack of normal cleaning, then a landlord has no right to any deposit deductions. Since HUD doesn’t have an official list of acceptable deductions, landlords have to go by their state rules (if any exist), personal experience, and their gut feeling.

Property Damage

If your tenant or their guests cause excessive damage to the property, you can use the security deposit toward repair or replacement. Some damage is fairly obvious, such as big holes in the wall or floor, or broken fixtures. Other conditions, not so immediately apparent, are also deductible from the security deposit.

These could include but not limited to:

Missing smoke or carbon monoxide detectors

Flea extermination, if a pet lived on the premises

Broken or missing window blinds

Appliances broken due to negligence.

Dirt and filth as a result of in adequate clean

Any damages caused by lack of common sense or improper use (like sliding down a stair handrail)

Even if you find some excessive damage after the deposit was returned, you can still send an invoice to the tenant. However, the chances of receiving that money is slim to none.

Cleaning

If you have to pick up and dispose of a few minor items after the tenant is gone, that’s not grounds to withhold part of the security deposit. And quite honestly, it’s just not worth the effort to deduct money for a few items. However, if the tenant left junk and trash all over the place, or food rotting in the fridge, that’s a different story.

Many leases specify that a tenant should leave

the property in “broom clean condition,”

or terms to that effect.

I’ve never really liked this term because a tenant could potentially sweep the apartment, but leave the stove, fridge, and closets a complete mess. Without more specific language in the lease, you’ll eventually regret using the term “broom clean”.

Painting

Many landlords repaint the interior of the rental property to attract a new tenant. It’s routine and usually performed every few years, so you can’t deduct the costs of hiring a painter or purchasing paint from the security deposit.

However, if the tenant painted the walls some hideous shade or drew “art” on them, the cost of repainting is deductible – but only for the affected rooms. The same holds true if the repainting is necessary because the tenant or guests smoked in the dwelling, causing staining on the walls.

Likewise, if the tenant painted without your permission (lease clause required), you would be able to deduct the cost of a painter and supplies to return the wall to its original color compared to when they moved in. Although, if the paint color is neutral and nicely executed, then you might want to consider thanking your tenant for painting!

Provide Receipts

Make sure to document all the necessary repair work to prove your expenses. In most states, such documentation is required above a fairly nominal monetary amount ($126 in California).

If you deducted money and the funds are unsubstantiated, the tenant may take you to small claims court. Many times, the tenant can be awarded 2-3 times the deposit amount if you wrongfully withheld anything.

By Glenn Curtis

Investopedia

Those who consistently make money in real estate know the market. They know the location and the history. They know what new developments are planned. They know the transportation and the schools. They know everything about the area where they invest. They have to know it all.

Staying ahead of the competition in real estate investment means doing your homework. If you are new to the business, it can be daunting, but in this article we’ll teach you five tricks that the old pros use to get ahead of the trends instead of chasing them.

Those who consistently make money in real estate know the market. They know the location and the history. They know what new developments are planned. They know the transportation and the schools. They know everything about the area where they invest. They have to know it all.

Staying ahead of the competition in real estate investment means doing your homework. If you are new to the business, it can be daunting, but in this article we’ll teach you five tricks that the old pros use to get ahead of the trends instead of chasing them. (To learn about the perks of real estate investing, see our Exploring Real Estate Investment Tutorial and Investing In Real Estate.)

Study Local Pricing

The first things to study are the current price trends in the area. For example, a potential investor should look to see if the price of homes is accelerating faster in one area than in others. Next, check to see if the average home price is more than in other neighboring towns. This will provide an idea of where the biggest demand is. Another reason to study these trends is that, over time, you will start to develop a sense for which prices are “fair” for certain properties and which are overpriced. For individuals looking to buy properties at the lowest cost possible, this knowledge can be invaluable.

Look for a Catalyst One sign that an area is up-and-coming and that it will be desirable in the future is the development of new infrastructure. When you see new roads and schools being built, it’s a sign that the community is set for a growth spurt. Investing in a growing community can be very profitable. In addition, certain types of development, like new shopping centers, may be extremely attractive to home buyers, and may also help keep the tax base low.

Spotting new developments can be as easy as looking out your car window as you drive by. Telltale signs of land clearing, surveying or the beginnings of construction in and around major roadways are pretty big tip-offs. Also, look for widening of traffic lanes, the installation of turnaround lanes and the erection of new traffic lights. All suggest the possibility of increased traffic flow.

Next, visit town hall at the municipality or the county level, and speak with the road and the building departments. They should be aware of any major projects slated to begin in the area, and they may even be able to provide you with a connection at the state level so you can find out if any state-owned roads or properties are slated for development as well. Real estate agents also have general idea of what new projects are about to be undertaken.

Explore Low-Tax Alternatives If there are two towns side by side – one with high property taxes (or with progressively rising property taxes) and the other with low property taxes – the one with the lower taxes will usually be more in demand.

Real estate agents can help you determine which areas have the best and worst tax structures. In addition, a simple call to the local tax assessor can reveal how much the town charges in taxes per $100 of house. The assessor can also let you know when the last time the area was evaluated by the township. Also watch to see if a reassessment is set to take place in the near future, as it may mean that property taxes are about to go up. Beware of towns and communities that are becoming overcrowded. Signs include schools filled to capacity and inferior roadways. This could mean the town will have to do some major construction to accommodate the influx of people. And how do they pay for that construction? Tax dollars.

Check the School Rankings Nearly every state ranks its schools by how well students in each district fare on tests in math and English. Sharp-eyed investors should look for schools that are moving up or are atop the list. These areas are often desirable to parents. Access to quality education is a big selling point to new home buyers.

There are several ways to find this information. Check our your state’s board of education website. Also, PSK12.com has public school rankings for most states in its free section. Visiting the schools yourself is also a good idea. Schools that rank the highest are usually quite eager to provide information.

Watch the Outskirts If the properties in a major city or town have become overpriced, the areas on the outer fringes most likely will soon be in demand. Areas in close proximity to major bus and rail transportation are even more desirable Nearly any area that is about to install a major train stop or a new major bus route will see its proverbial stock go up in value.

To find out what’s planned, you can check with the local railroad or bus company to see if they will be expanding service in the area. The local town hall or planning department will also have this information.

Bottom Line It pays to do your homework and to tap local resources to determine which areas are hot now and, more importantly, which ones will be hot in the future. Much of the information is out there and free for the taking. You just have to be willing to do the leg work.

Here are eight ways to help your home put its best face forward.

Homes with high curb appeal command higher prices and take less time to sell. We’re not talking about replacing vinyl siding with redwood siding; we’re talking about maintenance and beautifying tasks you’d like to live with anyway.

The way your house looks from the street — attractively landscaped and well-maintained — can add thousands to its value and cut the time it takes to sell. But which projects pump up curb appeal most? Some spit and polish goes a long way, and so does a dose of color.

Tip #1: Wash Your House’s Face

Before you scrape any paint or plant more azaleas, wash the dirt, mildew, and general grunge off the outside of your house. REALTORS® say washing a house can add $10,000 to $15,000 to the sale prices of some houses.

A bucket of soapy water and a long-handled, soft-bristled brush can remove the dust and dirt that have splashed onto your wood, vinyl, metal, stucco, brick, and fiber cement siding. Power washers (rental: $75 per day) can reveal the true color of your flagstone walkways.

Wash your windows inside and out, swipe cobwebs from eaves, and hose down downspouts. Don’t forget your garage door, which was once bright white. If you can’t spray off the dirt, scrub it off with a solution of 1/2 cup trisodium phosphate — TSP, available at grocery stores, hardware stores, and home improvement centers — dissolved in 1 gallon of water.

You and a friend can make your house sparkle in a few weekends. A professional cleaning crew will cost hundreds — depending on the size of the house and number of windows — but will finish in a couple of days.

Tip #2: Freshen the Paint Job

The most commonly offered curb appeal advice from real estate pros and appraisers is to give the exterior of your home a good paint job. Buyers will instantly notice it, and appraisers will value it. Of course, painting is an expensive and time-consuming facelift. To paint a 3,000-square-foot home, figure on spending $375 to $600 on paint; $1,500 to $3,000 on labor.

Your best bet is to match the paint you already have: Scrape off a little and ask your local paint store to match it. Resist the urge to make a statement with color. An appraiser will mark down the value of a house that’s painted a wildly different color from its competition.

Tip #3: Regard the Roof

The condition of your roof is one of the first things buyers notice and appraisers assess. Missing, curled, or faded shingles add nothing to the look or value of your house. If your neighbors have maintained or replaced their roofs, yours will look especially shabby.

You can pay for roof repairs now, or pay for them later in a lower appraisal; appraisers will mark down the value by the cost of the repair. According to the “2015 Remodeling Impact Report” from the NATIONAL ASSOCIATION OF REALTORS®, the national median cost of a new asphalt shingle roof is about $7,600.

Some tired roofs look a lot better after you remove 25 years of dirt, moss, lichens, and algae. Don’t try cleaning your roof yourself: call a professional with the right tools and technique to clean it without damaging it. A 2,000-square-foot roof will take a day and $400 to $600 to clean professionally.

Tip #4: Neaten the Yard

A well-manicured lawn, fresh mulch, and pruned shrubs boost the curb appeal of any home.

Replace overgrown bushes with leafy plants and colorful annuals. Surround bushes and trees with dark or reddish-brown bark mulch, which gives a rich feel to the yard. Put a crisp edge on garden beds, pull weeds and invasive vines, and plant a few geraniums in pots.

Green up your grass with lawn food and water. Cover bare spots with seeds and sod, get rid of crab grass, and mow regularly.

Tip #5: Add a Color Splash

Even a little color attracts and pleases the eye of would-be buyers.

Plant a tulip border in the fall that will bloom in the spring. Dig a flowerbed by the mailbox and plant some pansies. Place a brightly colored bench or Adirondack chair on the front porch. Get a little daring, and paint the front door red or blue.

These colorful touches won’t add to the value of our house: Appraisers don’t give you extra points for a blue bench. But beautiful colors enhance curb appeal and help your house to sell faster.

Tip #6: Glam Your Mailbox

An upscale mailbox, architectural house numbers, or address plaques can make your house stand out.

High-style die cast aluminum mailboxes range from $100 to $350. You can pick up a handsome, hand-painted mailbox for about $50. If you don’t buy new, at least give your old mailbox a facelift with paint and new house numbers.

These days, your local home improvement center or hardware stores has an impressive selection of decorative numbers. Architectural address plaques, which you tack to the house or plant in the yard, typically range from $80 to $200. Brass house numbers range from $3 to $11 each, depending on size and style.

Tip #7: Fence Yourself In

A picket fence with a garden gate to frame the yard is an asset. Not only does it add visual punch to your property, appraisers will give extra value to a fence in good condition, although it has more impact in a family-oriented neighborhood than an upscale retirement community.

Expect to pay $2,000 to $3,500 for a professionally installed gated picket fence 3 feet high and 100 feet long.

If you already have a fence, make sure it’s clean and in good condition. Replace broken gates and tighten loose latches.

Tip #8: Maintenance is a Must

Nothing looks worse from the curb — and sets off subconscious alarms — like hanging gutters, missing bricks from the front steps, or peeling paint. Not only can these deferred maintenance items damage your home, but they can decrease the value of your house by 10%.

Here are some maintenance chores that will dramatically help the look of your house:

Refasten sagging gutters.

Repoint bricks that have lost their mortar.

Reseal cracked asphalt.

Straighten shutters.

Replace cracked windows.

Environmental News

The RRP Rule seeks to reduce lead exposure from toxic lead dust that can be disturbed during renovations and repairs. The rule regulates lead-based paint activities, including renovation of residences built prior to 1978, and the certification of individuals and firms who are involved in these activities.The recordkeeping inspection conducted in October 2014 at Home Pro, a home renovation company, revealed that the company failed to obtain written acknowledgement from homeowners that they received a Renovate Right pamphlet prior to renovations, and to retain records documenting lead safe work practices.

Lead exposure can cause a range of adverse health effects, from behavioral disorders and learning disabilities to seizures and death, putting young children at the greatest risk because their nervous systems are still developing. A national survey of lead and allergens in housing conducted by HUD estimates that 38 million occupied housing units (about 40 percent of all housing units) in the United States contain some lead-based paint.

There are approximately 500,000 U.S. children ages 1-5 with blood lead levels above 5 micrograms per deciliter (µg/dL), the reference level at which the Centers for Disease Control recommends public health actions be initiated.

If you suspect the Lead Renovation, Repair and Painting (RRP) Rule has been violated at a recently completed or ongoing renovation project, EPA encourages you to contact Region 7 at 1-800-223-0425 or by using the electronic form available online.

by Brad McMillan

of Commonwealth Financial Network

Today, I want to revisit a post I wrote just over two years ago. I’ve updated some of the data, but the concerns and the conclusions remain timely. In keeping with one of my recurring themes, this is also an example of how rising interest rates won’t mark the end of the world but, rather, a return to a more normal environment.

Can the housing recovery survive rising interest rates?

That is, as rates rise, will we see average housing prices level off or even start to decline again?

This question is becoming increasingly relevant. Mortgage applications have fallen in some weeks recently as rates have risen, and the average mortgage rate just ticked back toward 4 percent, for the first time since the end of last year.

To keep this in perspective, rates are still at almost the lowest levels since records have been kept, per the chart below, and are still down significantly over the last year, despite the recent uptick.

Nonetheless, perception is reality, and buyers look at rates in the context of their recent experience.

Will an uptick in rates hurt demand?

At the end of the day, the future of housing depends on the market, on supply and demand. Let’s consider demand first; without it, supply is irrelevant.

It’s important to look at effective demand—demand from people who can afford to act. One way to analyze effective demand is to look at median incomes in order to determine how much people can afford to pay. We can then look at current mortgage rates and possible changes to determine how rate increases will impact effective buying power. Finally, we can compare the effective buying power with median home prices to see whether the change in rates changes effective demand, given current pricing.

Here’s an example: Assume a two-income family, with both husband and wife employed full time. The most recent data from the Bureau of Labor Statistics puts median weekly income for men over 25 at $944 and women at $759. This equates to a combined income of $1,703 per week, $7,380 per month, and $88,556 per year. At 28 percent of their income, a typical ratio, this family could afford to pay $2,066 per month on their mortgage. It’s a bit more complicated than that, of course, but this is a reasonable approximation.

Based on this payment, with a typical 30-year mortgage and a 20-percent down payment, this family could support the following mortgages and home purchase prices. You can see that higher rates do indeed affect the affordability of a home.

Rate Mortgage Purchase Price

3.5% $460,000 $575,000

4.0% $432,000 $540,000

4.5% $407,000 $508,000

5.0% $384,000 $480,000

5.5% $363,000 $453,000

6.0% $344,000 $430,000

The first thing I would note about these calculations is that no one in their right mind would actually borrow this much. These numbers represent what a borrower could conceivably qualify for, not what he or she should actually do. Nonetheless, they provide a guide to affordability overall.

The median price of a single-family home, depending on which data set you look at, is around $220,000, a nice round number. If we look at the figures above, we see that even at rates of 6 percent, affordability for the average family does not look to be a problem, even if rates continue to rise.

Taking a more restrictive view, using after-tax income, for example, we still find housing affordable at rates well above current levels. Using a 35-percent effective tax rate would give our family an allowed monthly mortgage payment of $1,343, which would lead to the following numbers:

Rate Mortgage Purchase Price

3.5% $299,000 $373,000

4.0% $281,000 $351,000

4.5% $265,000 $331,000

5.0% $250,000 $312,000

5.5% $236,000 $295,000

6.0% $224,000 $280,000

Even using this more conservative approach, the median house price remains affordable at higher interest rates.

Buying vs. renting

Another way to look at demand is to compare the relative costs of buying and renting. After all, just because a family can afford to buy doesn’t mean it will. What if it’s cheaper to rent?

Comparing the costs of renting versus owning is not simple; the numbers I have for the median apartment rental rate in the U.S. range between $801 and $1,430, depending on the source. For purposes of argument, let’s use the U.S. Census figure from 2011 for units built in the past four years, or $1,052. (Given rent increases since then, the rate is probably well above that, but it should be close enough.)

Using a 20-percent down payment and the median house price of $220,000, the monthly mortgage costs are as follows:

Rate Mortgage Payment

3.5% $176,000 $790

4.0% $176,000 $840

4.5% $176,000 $891

5.0% $176,000 $944

5.5% $176,000 $999

6.0% $176,000 $1,055

Even at the lowest average rent figure, a mortgage payment is comparable to rent using current interest rates. For the Census rent figure, mortgage payments will be less than rent for rates up to around 6 percent.

This is clearly a simplified analysis. I’m ignoring real estate taxes and maintenance costs, but I am also ignoring the mortgage interest tax deduction. I’m ignoring the freedom to move that comes with renting, but I am also ignoring the value of locking down housing costs into the indefinite future. Rents can go up; fixed mortgage payments don’t. Most of all, I’m ignoring the psychic benefits of homeownership, which haven’t gone away and which continued to drive people to buy, even when renting was cheaper.

The biggest thing I’m ignoring, however, is the down payment. The reason I’m not considering it is that the down payment has always, except for the period from 2005 to 2007 or so, been necessary. The need for a down payment is not a new factor but represents current conditions, and we do not need to model a change in this analysis.

Bottom line: demand should remain strong

In the end, buying demand for homes does not seem likely to be crippled by higher interest rates, at least in the immediate future. With a down payment, it is now generally cheaper to buy on a median basis and should continue to be so for some time, with all the other benefits of homeownership thrown in for free.

Given the amount of pent-up demand out there (look for another post on this soon) and the limited supply of homes available, it seems more likely than not that both demand and prices will continue to increase even if interest rates continue their climb.

Courtesy of Eric Jay TollReporter Phoenix Business Journal

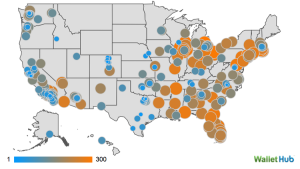

Eight Arizona cities are rising in the ranks of healthiest housing markets in the U.S., according to a WalletHub study. They all landed in the top 50 healthiest U.S. housing markets for comparably sized cities based on population.

Gilbert, a midsize city, ranked the highest of the Arizona cities at No. 11. Chandler was next at No. 22 and Tempe r

anked No. 28 in the midsize cities. Among large U.S. cities Mesa ranked No. 40 and Phoenix was No. 46.

The website consolidated rankings in 14 criteria, including pricing, percent of homes still under water, days on market, affordability, and other measures to determine the healthiest markets in the U.S.

Texas topped the healthiest markets list with No. 1 positions for Austin (large), Plano (midsize) and Frisco (small).

Other Western markets ranked high as well. Seattle (No. 2, large) and Denver (No. 3, large) ranked higher than all Arizona cities. Salt Lake City (No. 21, midsize), trailed Gilbert, but was just one ranking ahead of Chandler.

Rank of Arizona cities among healthiest U.S. residential real estate markets

11 Midsize – Gilbert

22 Midsize – Chandler

28 Midsize – Tempe

35 Midsize – Peoria

36 Midsize – Scottsdale

40 Large – Mesa

46 Large – Phoenix

49 Large – Tucson

55 Midsize – Glendale

88 Small – Surprise

123 Small – Yuma

Source: WalletHub

Courtesy of Mike SunnucksSenior Reporter Phoenix Business Journal

Phoenix home prices are up for a seventh straight month compared to year earlier, according to the much-watched Standard & Poor’s/Case-Shiller Home Price Index.

Phoenix’s growth rate in the most recent Case-Shiller report is 4.1 percent compared to a year earlier.

That is below the national average of 4.5 percent and trails hotter Western housing markets. Phoenix again has the lowest housing price growth rate among the nine Western cities in the Case-Shiller report.

Denver posted 10.2 percent growth in its home prices in June vs. June 2014, according to new Case-Shiller numbers out today.

That is the highest of the 20 large U.S. metro areas tracked in the index.

San Francisco is next at 9.5 percent followed by Dallas at 9.2 percent and Portland at 7.8 percent.

Denver and San Francisco previously have been the best-performing U.S. markets in the housing index.

Phoenix’s index growth is better than East Coast cities and Chicago but trails Los Angeles, Las Vegas and other Western housing markets.

Economists and real estate executives are not sure what impact stock market turmoil from Wall Street to China will have on real estate. It could discourage baby boomers and retirees from buying second and retirement homes if their portfolios are down. The declines also could reduce foreign investment, especially from Asia, in real estate.

Conversely, there could be a flight away from stocks to real estate if investors see safety in the latter.

City Housing price index growth rate (June 2015 vs. June 2016)

Phoenix: 4.1%

Denver: 10.2%

San Francisco: 9.5%

Dallas: 9.2%

Portland: 7.8%

Los Angeles: 6.3%

Las Vegas: 6.1%

Seattle: 7.4%

San Diego: 7.8%

Boston: 3.3%

D.C: 1.6%

Chicago: 1.4%

New York: 2.8%

U.S. average: 4.5%

Courtesy ofMike SunnucksSenior Reporter Phoenix Business Journal

Demand for rental homes remains strong in the Phoenix area.

Monthly rents are up and the supply of rental homes is down across metro Phoenix, according to Arizona State University economist and housing expert Michael Orr.

Orr, director of ASU’s Center for Real Estate Theory and Practice, said the average monthly rent for a single-family home is $1,548 up from $1,418 a year ago.

That’s a 9 percent increase.

Orr said there are very few lower rent homes on the market right now.The inventory of rental homes is also down from last year. Orr said there were more than 3,200 rental homes available in the local market in July. That compares to more than 4,200 a year earlier.

That is down 30 percent.

“Rental demand remains quite strong and supply is very constrained for properties below $1,300 a month,” Orr said.For the year, rents for homes were up 6.2 percent while apartments are up 10.9 percent. That translates into a 7 percent rise in rents across the market. Orr said continued demand for rental homes has landlords keeping those properties up for lease rather than put them for sale to home buyers.

“They keep raking in the money,” Orr said.

The ASU economist said that is contributing to fewer entry level homes on the market creating bidding wars from buyers.

High demand for single-family rentals also comes as the Joint Legislative Budget Council reports a decline new construction permits for apartments.

Courtesy of

Courtesy of  Courtesy of

Courtesy of  Courtesy of

Courtesy of